Bank Management - Introduction

A bank is a financial institution which accepts deposits, pays interest on pre-defined rates, clears checks, makes loans, and often acts as an intermediary in financial transactions. It also provides other financial services to its customers.

Bank management governs various concerns associated with bank in order to maximize profits. The concerns broadly include liquidity management, asset management, liability management and capital management. We will discuss these areas in later chapters.

Origin of Banks

The origin of bank or banking activities can be traced to the Roman empire during the Babylonian period. It was being practiced on a very small scale as compared to modern day banking and frame work was not systematic.

Modern banks deal with banking activities on a larger scale and abide by the rules made by the government. The government plays a crucial role with its control over the banking system. This calls for bank management, which further ensures quality service to customers and a win-win situation between the customer, the banks and the government.

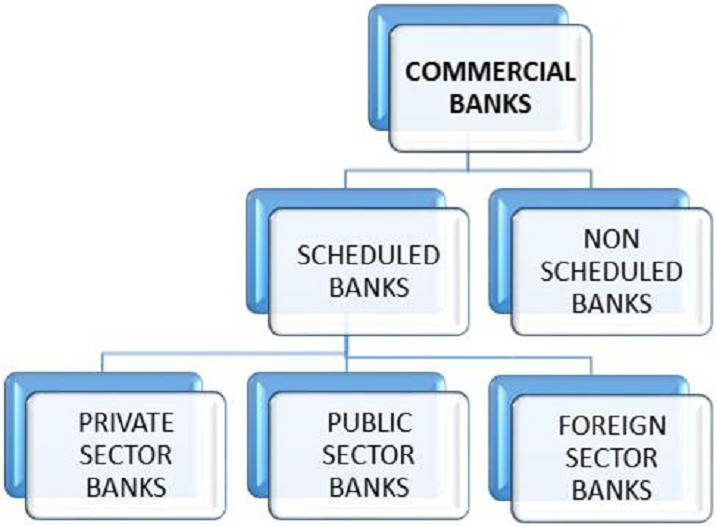

Scheduled & Non-Scheduled Banks

Scheduled and non-scheduled banks are categorized by the criteria or eligibility setup by the governing authority of a particular region. The following are the basic differences between scheduled and nonscheduled banks in the Indian banking perspective.

Scheduled banks are those that have paid-up capital and deposits of an aggregate value of not less than rupees five lakhs in the Reserve Bank of India. All their banking businesses are carried out in India. Most of the banks in India fall in the scheduled bank category.

Non-scheduled banks are the banks with reserve capital of less than five lakh rupees. There are very few banks that fall in this category.

Evolution of Banks

Banking system has evolved from barbaric banking where commodities were loaned to modern day banking system, which caters to a range of financial services. The evolution of banking system was gradual with growth in each and every aspect of banking. Some of the major changes which took place are as follows −

- Barter system replaced by money which made transaction uniform

- Uniform laws were setup to increase public trust

- Centralized banks were setup to govern other banks

- Book keeping was evolved from papers to digital format with the introduction of computers

- ATMs were setup for easier withdrawal of funds

- Internet banking came into existence with development of internet

Banking system has witnessed unprecedented growth and will be undergoing it in future too with the advancement in technology.

Growth of Banking System in India

The journey of banking system in India can be put into three different phases based on the services provided by them. The entire evolution of banking can be described in these distinct phases −

Phase 1

This was the early phase of banking system in India from 1786 to 1969. This period marked the establishment of Indian banks with more banks being set up. The growth was very slow in this phase and banking industry also experienced failures between 1913 to 1948.

The Government of India came up with the banking Companies Act in 1949. This helped to streamline the functions and activities of banks. During this phase, public had lesser confidence in banks and post offices were considered more safe to deposit funds.

Phase 2

This phase of banking was between 1969 to 1991, there were several major decisions being made in this phase. In 1969, fourteen major banks were nationalized. Credit Guarantee Corporation was created in 1971. This helped people avail loans to set up businesses.

In 1975, regional rural banks were created for the development of rural areas. These banks provided loans at lower rates. People started having enough faith and confidence on the banking system, and there was a plunge in the deposits and advances being made.

Phase 3

This phase came into existence from 1991. The year 1991 marked the beginning of liberalization, and various strategies were implemented to ensure quality service and improve customer satisfaction.

The ongoing phase witnessed the launch of ATMs which made cash withdrawals easier. This phase also brought in Internet banking for easier financial transactions from any part of world. Banks have been making attempts to provide better services and make financial transactions faster and efficient.

Bank Management - Commercial Banking

A commercial bank is a type of financial institution that provides services like accepting deposits, making business loans, and offering basic investment products. The term commercial bank can also refer to a bank, or a division of a large bank, which precisely deals with deposits and loan services provided to corporations or large or middle-sized enterprises as opposed to individual members of the public or small enterprises. For example, Retail banking, or Merchant banks.

A commercial bank can also be defined as a financial institution that is licensed by law to accept money from different enterprises as well as individuals and lend money to them. These banks are open to the mass and assist individuals, institutions, and enterprises.

Basically, a commercial bank is the type of bank people tend to use regularly. They are formulated by federal and state laws on the basis of the coordination and the services they provide.

These banks are controlled by the Federal Reserve System. A commercial bank is licensed to assist the following functions −

- Accept deposits − Receiving money from individuals and enterprises known as depositors.

- Dispense payments − Making payments according to the convenience of the depositors. For example, honoring a check.

- Collections − Bank plays as an agent to collect funds from another banks receivable to the depositor. For example, when someone pays through check drawn on an account from a different bank.

- Invest funds − Contributing or spending money in securities for making more money. For example, mutual funds.

- Safeguard money − A bank is regarded as a safe place to store wealth including jewelry and other assets.

- Maintain savings − The money of the depositors is maintained, and the accounts are checked and on a regular basis.

- Maintain custodial accounts − These accounts are maintained under the supervision of one person but are actually for the benefit of another person.

- Lend money − Lending money to companies, depositors in case of some emergency.

Commercial banks are apparently the largest source of financing for private capital investment in a nation, especially, like India. A capital investment can be defined as the purchase of a property with the purpose of either producing income from the property, increasing the value of the property over time, or both. Similar capital purchases made by enterprises may involve things like plants, tools and equipment.

Present Structure

The current banking framework in India can be broadly classified into two. The first classification divides banks into three sub-categories — the Reserve Bank of India, commercial banks and cooperative banks.

The second divides the banks into two sub-categories — scheduled banks and non-scheduled banks. In both of these systems of categorization, the RBI, is the head of the banking structure. It monitors and holds all the reserve capital of all the commercial or scheduled banks across the nation.

Commercial banks are the foundations that receive deposits from individuals and enterprises and lend loans to them. They generate credit. Commercial banks in India are regulate under the Banking Regulation Act of 1949. These banks are further categorized as −

- Scheduled banks

- Non-scheduled banks

Scheduled banks are banks which are listed in the 2nd schedule of the Reserve Bank of India Act, 1934. Non-scheduled banks are those banks which are not listed in the second schedule of the Reserve Bank of India Act,1934.

Scheduled Banks

In India, for a bank to qualify as a scheduled bank, it needs to meet the criteria as underplayed by the Reserve Bank of India. The following is a list of the criterions

- The banks should carry all their business transactions in India.

- All schedule banks are bound to hold a capital of not less than rupees five lakhs in the Reserve Bank of India.

- In the year 2011, five lakhs rupees calculated in terms of dollars amounted to $11,156.

Thus, any commercial, cooperative, nationalized, foreign bank and any other banking foundation that accepts and satisfies these set conditions are termed as scheduled banks but not all schedule banks are commercial banks.

The scheduled commercial banks are those banks which are included in the second schedule of RBI Act, 1934. These banks accept deposits, lend loans and also offer other banking services. The major difference between scheduled commercial banks and scheduled cooperative banks is their holding pattern. Cooperative banks are registered as cooperative credit institutions under the Cooperative Societies Act of 1912.

Scheduled banks are further categorized as −

- Private-sector banks

- Public sector banks

- Foreign sector banks

Private-Sector Banks

These banks acquire larger parts of stake or congruity is maintained by the private shareholders and not by government. Thus, banks where maximum amount of capital is in private hands are considered as private-sector banks. In India, we have two types of private-sector banks −

- Old Private-Sector Banks

- New Private-Sector Banks

Old Private-sector Banks

The old private-sector banks were set up before nationalization in 1969. They had their own independence. These banks were either too small or specialist to be incorporated in nationalization. The following is a list of old private-sector banks in India −

- Catholic Syrian Bank

- City Union Bank

- Dhanlaxmi Bank

- Federal Bank ING

- Vysya Bank

- Jammu and Kashmir Bank

- Karnataka Bank

- Karur Vysya Bank

- Lakshmi Vilas Bank

- Nainital Bank

- Ratnakar Bank

- South Indian Bank

- Tamilnadu Mercantile Bank

From the above mentioned banks, the Nainital Bank is an auxiliary or branch of the Bank of Baroda, which has 98.57% stake in it. A few old generation private-sector banks merged with other banks. For example, in the year 2007, Lord Krishna Bank merged with Centurion Bank of Punjab. Sangli Bank merged with ICICI Bank in 2006. Yet again, Centurion Bank of Punjab merged with HDFC in 2008.

New Private-sector Banks

Banks which started their operations after liberalization in the 1990s are the new private-sector banks. These banks were permitted entry into the Indian banking sector after the amendment of the Banking Regulation Act in 1993.

At present, the following new private-sector banks are operational in India −

- Axis Bank Development

- Credit Bank (DCB Bank Ltd)

- HDFC Bank

- ICICI Bank

- IndusInd Bank

- Kotak Mahindra Bank

- Yes Bank

In addition to these seven banks, there are two more banks which are yet to commence operation. They got the ‘in-principle’ licenses from RBI. These two banks are IDFC and Bandhan Bank of Bandhan Financial Services.

Commercial Banking Functions

Commercial banking is basically the parent of all types of banking available in the present banking structure. In order to understand the role of commercial banking, let us discuss some of its major functions. The following are the major functions of commercial banks −

Acceptance of Deposits

The most important task of commercial banks is to accept deposits from the public. Banks maintain and keep records of all the demand deposit accounts of their customers and transform the deposit money into cash, vice versa is also possible as per the requirements of the customers. Technically, demand deposits are accepted in current accounts. The depositor can withdraw deposited money anytime by means of checks.

In fixed deposit accounts, the depositor can withdraw the money deposited only after a certain period. We can say, fixed deposits are time liabilities of the banks. Deposits in the saving bank accounts are subjected to certain limitations regarding the amount one can receive and withdraw. In this way, banks collect savings from people and maintain a reserve of these savings.

Giving Loans and Advances

One of the most important functions of commercial banks is to extend loans and advances out of the money through deposits of businessmen and entrepreneurs against permitted securities and safety like gold or silver bullion, government securities, easily saleable stocks and shares and marketable goods.

Banks give advances to customers or depositors through overdrafts, discounting bills, money-at-call and short notice, loans and advances, different forms of direct loans to traders and producers.

Using Check System

Banks facilitate services through some medium of exchange like checks. Using checks for settling debts in business transaction is always preferred over cash. Check is also referred as the most developed credit instrument.

There are some other major functions of commercial banking. They perform a multitude of other non-banking operations. These non-banking operations are further classified as agency services and general utility services.

Agency Services

The services banks ensure for and on behalf of their customers are agency services. The banks play the role of an executor, trustee and attorney for the customer’s will. They accumulate as well as make payments for bills, checks, promissory notes, interests, dividends, rents, subscriptions, insurance premium, policy etc.

As mentioned above, they provide services for and on behalf of customers and also issue drafts, mail, telegraphic transfers on behalf of clients to remit funds. They also help their customers by arranging income-tax professionals to facilitate the process of income tax returns. Basically the bankers work as correspondents, agents or representatives of their clients.

General Utility Services

The services ensured for the entire society are known as general utility services. The bankers issue bank drafts and traveler’s checks to facilitate transfer of funds from one part of the country to another. They give the customers letters of credit which help them when they go abroad.

They handle foreign exchange or finance foreign trade by accepting or assembling foreign bills of exchange. Banks arrange for safe deposit vaults where the customers can secure their valuables. Banks also assemble statistics and business information relevant to trade, commerce and industry.

Commercial Banking Reforms

The Indian government decided to amend new economic reforms. Earlier, the banking industry was highly dominated by the public sector. This lead to profitability and poor asset quality. The country was undergoing deep economic crisis. The main aim of the banking sector reforms was to build a diversified, efficient and competitive financial system. The ultimate goal of this system was to properly allocate resources through functional flexibility, improved financial viability and institutional strengthening.

The reforms are mainly focused towards eradicating financial repression through minimizations in statutory preemptions, while concurrently stepping up prudential regulations. In addition to this, interest rates on deposits and the loans lent by banks had been progressively denationalized.

By the year 1991, India had nationalized banks in two phases in 1969 and 1980. The public sector banks (PSBs) controlled the credit supply. The post-1991 period saw three different chronological phases. The first phase was roughly between 1991 to 1998. The second phase started in 1998 and continued until the beginning of global financial crisis. The third phase is the ongoing one.

Phase 1

As we know post-1991 was a period of structural reforms in the financial sector. There was unprecedented development in various areas such as banking and capital markets. These reforms were based on the recommendations put forward by the Narasimham Committee in their report in November 1991.

After the first phase of banking sector reforms under the guidance of Narasimham Committee the following measures were undertaken by government −

Lowering SLR and CRR

The high SLR and CRR minimized the profits of the banks. The SLR was minimized from 38.5% in 1991 to 25% in 1997. As a result, banks were left with more funds that could be allocated to agriculture, industry, trade etc.

The Cash Reserve Ratio (CRR) is a bank’s cash ratio of total deposits to be maintained with RBI. The CRR has been lowered from 15% in 1991 to 4.1% in June 2003. The aim is to release the funds locked up with RBI.

Prudential Norms

These norms were initiated by RBI in order to bring in professionalism in commercial banks. The main objective of these norms were proper disclosure of income, classification of assets and provision for bad debts so as to assure that the books of commercial banks mirrored the accurate and correct picture of financial position.

Prudential norms ensured the banks made 100% provision for all non-performing assets (NPAs). For this purpose, sponsoring was placed at Rs.10,000 crores phased over 2 years.

Capital Adequacy Norms (CAN)

It is the ratio of minimum capital to risk asset ratio. In April 1992, RBI fixed CAN at 8%. By March 1996, all public sector banks had attained the ratio of 8%.

Deregulation of Interest Rates

The Narasimham Committee recommended that interest rates should be determined by market forces. From 1992, determining interest rates has become more simple and easy.

Recovery of Debts

The government of India issued the “Recovery of debts due to Banks and Financial Institutions Act 1993” in order to support and speed up the recovery of the dues of banks and financial institutions. Six Special Recovery Tribunals have been established to work on the same. An Appellate Tribunal was also established in Mumbai.

Competition from New Private-Sector Banks

Today banking is open to private-sector. New private-sector banks have already started functioning well in the banking industry. These new private-sector banks are permitted to hike capital contribution from foreign institutional investors up to 20% and from NRIs up to 40%. As a result, there is an increase in competition.

Phasing Out of Directed Credit

The committee recommended phasing out of the directed credit plans. A recommendation was made to lower the credit target for the priority sector from 40% to 10%. It would be very difficult for the government as farmers, small industrialists and transporters have powerful lobbies.

Access to Capital Market

The Banking Companies (Accusation and Transfer of Undertakings Act) was enhanced to allow the banks to increase capital through public issues. This is subject to a provision that the holding of central government would not decrease below 51% of paid-up-capital. The State Bank of India has already increased substantial amount of funds through equity and bonds.

Freedom of Operation

Scheduled commercial banks are given freedom to open new branches and upgrade extension counters, after attaining capital adequacy ratio and prudential accounting norms. The banks are also permitted to close non-viable branches other than in rural areas.

Local Area banks (LABs)

In 1996, RBI issued guidelines for establishing Local Area Banks and it approved to build 7 LABs in private-sector. LABs provide support in mobilizing rural savings and in converting them to investment in local areas.

Supervision of Commercial Banks

The RBI formed a Board of financial Supervision with an advisory Council to empower the supervision of banks and financial institutions. In 1993, RBI established a new department, the Department of Supervision, as an independent unit for supervision of commercial banks.

Measures were taken to empower capital infusion by the government to approximately Rs. 20,000 Crore. Along with this, public sector banks were permitted to access the capital markets for infusion of equity capital subject to the condition that government ownership would remain at least at 51 percent.

Also, necessary measures were taken to develop the fragile health and low profitability. This called for adherence to internationally acceptable prudential norms, asset classification and provisioning and capital adequacy. Many measures were also started, the prominent one being the enactment of The Recovery of Debts Due to Banks and Financial Institutions Act in 1993. Following this, 29 debt recovery tribunals (DRTs) and five debt recovery appellate tribunals (DRATs) were established at a number of places in the country.

All these measures minimized the percentage of NPAs to gross advances from 23.2 percent in March 1993 to 16 percent in March 1998. Later rationalization and deregulation of interest rates was also undertaken.

Concurrently, in order to build competition within the banking sphere, different measures were undertaken. These comprised of opening private-sector banks, greater freedom to open branches and installation of ATMs, and full functional freedom to banks to evaluate working capital requirements.

Phase 2

The second phase of reforms begun with another Narasimham Committee report in April 1998, which succeeded the East Asian Crisis. Post 1998, a need was felt to restructure debt as the DRTs process was very slow because of many legal and other hurdles.

An important feature in this phase was the growing competition between banks. Though 21 new banks including four private-sector banks, one public sector bank and 16 foreign entities enrolled, the overall scheduled commercial banks (SCB) decreased approximately four-fifths to 82 by 2007. In addition to this, FDI in the banking sector was brought under the automatic route, and the limit in private-sector banks was increased from 49 percent to 74 percent in 2004.

In order to make banking sector stronger, the government delegated a Committee on banking sector reforms under the Chairmanship of M. Narasimham. It endured its report in April 1998. The Committee focused mainly on structural measures and development in standards of disclosure and levels of transparency.

The following reforms were undertaken on the recommendations made by the committee −

- New Areas − New areas for bank financing have been unclosed like Insurance, credit cards, asset management, leasing, gold banking, investment banking etc.

- New Instruments − For more flexibility and better risk management new tools and technologies have been introduced. These instruments include interest rate swaps, cross currency forward contracts, forward rate agreements, liquidity adjustment facility for meeting day-to-day liquidity mismatch.

- Risk Management − Banks have initialized specialized committees to assess various risks. Their Skills and systems are upgraded on a regular basis.

- Strengthening Technology − Technology infrastructure has been reinforced for payment and settlement with services such as electronic funds transfer, centralized fund management system, etc.

- Increase Inflow of Credit − Measures are taken to boost up the flow of credit to priority sector by focusing on Micro Credit and Self Help Groups.

- Increase in FDI Limit − The limit for FDI has been increased in private-sector banks from 49% to 74%.

- Universal banking − It refers to the merging of commercial banking and investment banking. There are a few guidelines for the expansion of universal banking.

- Adoption of Global Standards − The RBI recently introduced risk based supervision of banks. Best international exercises in accounting systems, corporate governance, payment and settlement systems etc. are being endorsed.

- Information Technology − Banks have proposed online banking, E-banking, Internet banking, telephone banking etc. Measures have been taken to support delivery of banking services via electronic channels.

- Management of NPAs − Measures were taken by RBI and central government for management of non-performing assets (NPAs), like corporate Debt Restructuring (CDR), Debt Recovery Tribunals (DRTs) and Lok Adalats.

- Mergers and Amalgamation − In May 2005, RBI issued guidelines for merger and Amalgamation of private-sector banks.

- Guidelines for Anti-Money Laundering − Recently, prevention of money laundering was given importance in international financial relationships. In 2004, RBI updated the guidelines on know your customer (KYC) principles.

- Managerial Autonomy − In February 2005, the Government of India circulated a managerial autonomy package for public sector banks to supply them a level playing field with private-sector banks in India.

- Customer Service − Past years witnessed improvement in customer service. The RBI advanced its services with credit card facilities, banking ombudsman, settlement of claims of deceased depositors etc.

- Base Rate System of Interest Rates − The system of Benchmark Prime Lending Rate (BPLR) was introduced in 2003 to ensure true reflection of the actual costs. The RBI proposed the system of Base Rate on 1st July, 2010. The base rate can be defined as the minimum rate for all loans. If we take banking system as a whole, the base rates were in the range of 5.50% - 9.00% as on 13th October, 2010.

The Banking Sector Reform Committee further recommended that presence of a healthy competition between public sector banks and private-sector banks was important. The report showed flow of capital to meet higher and unspecified levels of capital adequacy and minimization of targeted credit.

The government focused with the help of reform process on improving the role of market forces by making sharp reduction in preemption through reserve requirement, market determined pricing for government securities, disbanding of administered interest rates with a few exceptions and improved transparency and disclosure norms to support market discipline.

Bank Management - Liquidity

Liquidity in banking refers to the ability of a bank to meet its financial obligations as they come due. It can come from direct cash holdings in currency or on account at the Federal Reserve or other central bank. More frequently, it comes from acquiring securities that can be sold quickly with minimal loss. This basically states highly creditworthy securities, comprising of government bills, which have short term maturities.

If their maturity is short enough the bank may simply wait for them to return the principle at maturity. For short term, very safe securities favor to trade in liquid markets, stating that large volumes can be sold without moving prices too much and with low transaction costs.

Nevertheless, a bank’s liquidity condition, particularly in a crisis, will be affected by much more than just this reserve of cash and highly liquid securities. The maturity of its less liquid assets will also matter. As some of them may mature before the cash crunch passes, thereby providing an additional source of funds.

Need for Liquidity

We are concerned about bank liquidity levels as banks are important to the financial system. They are inherently sensitive if they do not have enough safety margins. We have witnessed in the past the extreme form of damage that an economy can undergo when credit dries up in a crisis. Capital is arguably the most essential safety buffer. This is because it supports the resources to reclaim from substantial losses of any nature.

The closest cause of a bank’s demise is mostly a liquidity issue that makes it impossible to survive a classic “bank run” or, nowadays, a modern equivalent, like an inability to approach the debt markets for new funding. It is completely possible for the economic value of a bank’s assets to be more than enough to wrap up all of its demands and yet for that bank to go bust as its assets are illiquid and its liabilities have short-term maturities.

Banks have always been reclining to runs as one of their principle social intentions are to perform maturity transformation, also known as time intermediation. In simple words, they yield demand deposits and other short term funds and lend them back out at longer maturities.

Maturity conversion is useful as households and enterprises often have a strong choice for a substantial degree of liquidity, yet much of the useful activity in the economy needs confirmed funding for multiple years. Banks square this cycle by depending on the fact that households and enterprises seldom take advantage of the liquidity they have acquired.

Deposits are considered sticky. Theoretically, it is possible to withdraw all demand deposits in a single day, yet their average balances show remarkable stability in normal times. Thus, banks can accommodate the funds for longer durations with a fair degree of assurance that the deposits will be readily available or that equivalent deposits can be acquired from others as per requirement, with a raise in deposit rates.

How Can a Bank Achieve Liquidity

Large banking groups engage themselves in substantial capital markets businesses and they have considerable added complexity in their liquidity requirements. This is done to support repo businesses, derivatives transactions, prime brokerage, and other activities.

Banks can achieve liquidity in multiple ways. Each of these methods ordinarily has a cost, comprising of −

- Shorten asset maturities

- Improve the average liquidity of assets

- Lengthen

- Liability maturities

- Issue more equity

- Reduce contingent commitments

- Obtain liquidity protection

Shorten asset maturities

This can assist in two fundamental ways. The first way states that, if the maturity of some assets is shortened to an extent that they mature during the duration of a cash crunch, then there is a direct benefit. The second way states that, shorter maturity assets are basically more liquid.

Improve the average liquidity of assets

Assets that will mature over the time horizon of an actual or possible cash crunch can still be crucial providers of liquidity, if they can be sold in a timely manner without any redundant loss. Banks can raise asset liquidity in many ways.

Typically, securities are more liquid than loans and other assets, even though some large loans are now framed to be comparatively easy to sell on the wholesale markets. Thus, it is an element of degree and not an absolute statement. Mostly shorter maturity assets are more liquid than longer ones. Securities issued in large volume and by large enterprises have greater liquidity, because they do more creditworthy securities.

Lengthen liability maturities

The longer duration of a liability, the less it is expected that it will mature while a bank is still in a cash crunch.

Issue more equity

Common stocks are barely equivalent to an agreement with a perpetual maturity, with the combined benefit that no interest or similar periodic payments have to be made.

Reduce contingent commitments

Cutting back the amount of lines of credit and other contingent commitments to pay out cash in the future. It limits the potential outflow thus reconstructing the balance of sources and uses of cash.

Obtain liquidity protection

A bank can scale another bank or an insurer, or in some cases a central bank, to guarantee the connection of cash in the future, if required. For example, a bank may pay for a line of credit from another bank. In some countries, banks have assets prepositioned with their central bank that can further be passed down as collateral to hire cash in a crisis.

All the above mentioned techniques used to achieve liquidity have a net cost in normal times. Basically, financial markets have an upward sloping yield curve, stating that interest rates are higher for long-term securities than they are for short-term ones.

This is so mostly the case that such a curve is referred as normal yield curve and the exceptional periods are known as inverse yield curves. When the yield curve has a top oriented slope, contracting asset maturities decreases investment income while extending liability maturities raises interest expense. In the same way, more liquid instruments have lower yields, else equal, minimizing investment income.

Bank Mngmt - Liquidity Management Theory

There are probable contradictions between the objectives of liquidity, safety and profitability when linked to a commercial bank. Efforts have been made by economists to resolve these contradictions by laying down some theories from time to time.

In fact, these theories monitor the distribution of assets considering these objectives. These theories are referred to as the theories of liquidity management which will be discussed further in this chapter.

Commercial Loan Theory

The commercial loan or the real bills doctrine theory states that a commercial bank should forward only short-term self-liquidating productive loans to business organizations. Loans meant to finance the production, and evolution of goods through the successive phases of production, storage, transportation, and distribution are considered as self-liquidating loans.

This theory also states that whenever commercial banks make short term self-liquidating productive loans, the central bank should lend to the banks on the security of such short-term loans. This principle assures that the appropriate degree of liquidity for each bank and appropriate money supply for the whole economy.

The central bank was expected to increase or erase bank reserves by rediscounting approved loans. When business started growing and the requirements of trade increased, banks were able to capture additional reserves by rediscounting bills with the central banks. When business went down and the requirements of trade declined, the volume of rediscounting of bills would fall, the supply of bank reserves and the amount of bank credit and money would also contract.

Advantages

These short-term self-liquidating productive loans acquire three advantages. First, they acquire liquidity so they automatically liquidate themselves. Second, as they mature in the short run and are for productive ambitions, there is no risk of their running to bad debts. Third, such loans are high on productivity and earn income for the banks.

Disadvantages

Despite the advantages, the commercial loan theory has certain defects. First, if a bank declines to grant loan until the old loan is repaid, the disheartened borrower will have to minimize production which will ultimately affect business activity. If all the banks pursue the same rule, this may result in reduction in the money supply and cost in the community. As a result, it makes it impossible for existing debtors to repay their loans in time.

Second, this theory believes that loans are self-liquidating under normal economic circumstances. If there is depression, production and trade deteriorate and the debtor fails to repay the debt at maturity.

Third, this theory disregards the fact that the liquidity of a bank relies on the salability of its liquid assets and not on real trade bills. It assures safety, liquidity and profitability. The bank need not depend on maturities in time of trouble.

Fourth, the general demerit of this theory is that no loan is self-liquidating. A loan given to a retailer is not self-liquidating if the items purchased are not sold to consumers and stay with the retailer. In simple words a loan to be successful engages a third party. In this case the consumers are the third party, besides the lender and the borrower.

Shiftability Theory

This theory was proposed by H.G. Moulton who insisted that if the commercial banks continue a substantial amount of assets that can be moved to other banks for cash without any loss of material. In case of requirement, there is no need to depend on maturities.

This theory states that, for an asset to be perfectly shiftable, it must be directly transferable without any loss of capital loss when there is a need for liquidity. This is specifically used for short term market investments, like treasury bills and bills of exchange which can be directly sold whenever there is a need to raise funds by banks.

But in general circumstances when all banks require liquidity, the shiftability theory need all banks to acquire such assets which can be shifted on to the central bank which is the lender of the last resort.

Advantage

The shiftability theory has positive elements of truth. Now banks obtain sound assets which can be shifted on to other banks. Shares and debentures of large enterprises are welcomed as liquid assets accompanied by treasury bills and bills of exchange. This has motivated term lending by banks.

Disadvantage

Shiftability theory has its own demerits. Firstly, only shiftability of assets does not provide liquidity to the banking system. It completely relies on the economic conditions. Secondly, this theory neglects acute depression, the shares and debentures cannot be shifted to others by the banks. In such a situation, there are no buyers and all who possess them want to sell them. Third, a single bank may have shiftable assets in sufficient quantities but if it tries to sell them when there is a run on the bank, it may adversely affect the entire banking system. Fourth, if all the banks simultaneously start shifting their assets, it would have disastrous effects on both the lenders and the borrowers.

Anticipated Income Theory

This theory was proposed by H.V. Prochanow in 1944 on the basis of the practice of extending term loans by the US commercial banks. This theory states that irrespective of the nature and feature of a borrower’s business, the bank plans the liquidation of the term-loan from the expected income of the borrower. A term-loan is for a period exceeding one year and extending to a period less than five years.

It is admitted against the hypothecation (pledge as security) of machinery, stock and even immovable property. The bank puts limitations on the financial activities of the borrower while lending this loan. While lending a loan, the bank considers security along with the anticipated earnings of the borrower. So a loan by the bank gets repaid by the future earnings of the borrower in installments, rather giving a lump sum at the maturity of the loan.

Advantages

This theory dominates the commercial loan theory and the shiftability theory as it satisfies the three major objectives of liquidity, safety and profitability. Liquidity is settled to the bank when the borrower saves and repays the loan regularly after certain period of time in installments. It fulfills the safety principle as the bank permits a relying on good security as well as the ability of the borrower to repay the loan. The bank can use its excess reserves in lending term-loan and is convinced of a regular income. Lastly, the term-loan is highly profitable for the business community which collects funds for medium-terms.

Disadvantages

The theory of anticipated income is not free from demerits. This theory is a method to examine a borrower’s creditworthiness. It gives the bank conditions for examining the potential of a borrower to favorably repay a loan on time. It also fails to meet emergency cash requirements.

Liabilities Management Theory

This theory was developed further in the 1960s. This theory states that, there is no need for banks to lend self-liquidating loans and maintain liquid assets as they can borrow reserve money in the money market whenever necessary. A bank can hold reserves by building additional liabilities against itself via different sources.

These sources comprise of issuing time certificates of deposit, borrowing from other commercial banks, borrowing from the central banks, raising of capital funds through issuing shares, and by ploughing back of profits. We will look into these sources of bank funds in this chapter.

Time Certificates of Deposits

These deposits have different maturities ranging from 90 days to less than 12 months. They are transferable in the money market. Thus, a bank can have connection to liquidity by selling them in the money market. But this source has two demerits.

First, if during a crisis, the interest rate layout in the money market is higher than the ceiling rate set by the central bank, time deposit certificates cannot be sold in the market. Second, they are not reliable source of funds for the commercial banks. Bigger commercial banks have a benefit in selling these certificates as they have large certificates which they can afford to sell at even low interest rates. So the smaller banks face trouble in this respect.

Borrowing from other Commercial Banks

A bank may build additional liabilities by borrowing from those banks that have excess reserves. But these borrows are only for a very short time, that is for a day or at the most for a week.

The interest rate of these types of borrowings relies on the controlling price in the money market. But borrowings from other banks are only possible when the economic conditions are normal economic. In abnormal times, no bank can afford to grant to others.

Borrowing from the Central Bank

Banks also build liabilities on themselves by borrowing from the central bank of the country. They borrow to satisfy their liquidity requirements for short-term and by discounting bills from the central bank. But these types of borrowings are comparatively costlier than borrowings from other sources.

Raising Capital Funds

Commercial banks hold funds by distributing fresh shares or debentures. But the availability of funds through these sources relies on the volume of dividend or interest rate which the bank is prepared to pay. Basically banks are not prepared to pay rates more than paid by manufacturing and trading enterprises. Thus they fail to get enough funds from these sources.

Ploughing Back Profits

The ploughing back of its profits is considered as an alternative source of liquid funds for a commercial bank. But how much it can obtain from this source relies on its rate of profit and its dividend policy. Larger banks can depend on these sources rather than the smaller banks.

Functions of Capital Funds

Generally, bank capital comprises of own sources of asset finances. The volume of capital is equivalent to the net assets worth, marking the margin by which assets outweigh liabilities.

Capital is expected to secure a bank from all sorts of uninsured and unsecured risks suitable to transform into losses. Here, we obtain two principle functions of capital. The first function is to capture losses and the second is to establish and maintain confidence in a bank.

The different functions of capital funds are briefly described in this chapter.

The Loss Absorbing Function

Capital is required to permit a bank to cover any losses with its own funds. A bank can keep its liabilities completely enclosed by assets as long as its sum losses do not deplete its capital.

Any losses sustained minimize a bank’s capital, set off across its equity products like share capital, capital funds, profit-generated funds, retained earnings, relying on how its general assembly decides.

Banks take good care to fix their interest margins and other spreads between the income derived from and the price of borrowed funds to enclose their ordinary expenses. That is why operating losses are unlikely to subside capital on a long-term basis. We can also say that banks with a long and sound track record owing to their past efficiency, have managed to produce enough amount of own funds to easily cope with any operating losses.

For a new bank without much of a success history, operating losses may conclude driving capital below the minimum level fixed by law. Banks run a probable and greater risk of losses coming from borrower defaults, rendering some of their assets partly or completely irrecoverable.

The Confidence Function

A bank may have sufficient assets to back its liabilities, and also adequate capital power which balances deposits and other liabilities by assets. This generates a financial flow in the ordinary course of banking business. Here, it is an important necessity that a bank’s capital covers its fixed investments like fixed assets, involving interests in subsidiaries. These are used in its business operation, which basically generate no financial flow.

If the cash flow generated by assets falls short of meeting deposit calls or other due liabilities, it is not difficult for a bank with sufficient capital backing and credibility to get its missing liquidity on the interbank market. Other banks will not feel uncomfortable lending to it, as they are aware of the capacity to conclude its liabilities with its assets.

This type of bank can withstand a major deposit flight and refinance it with interbank market borrowings. In banks with a sufficient capital base, anyhow, there is no reason to fear a mass-scale depositor exodus. The logic is that the issues which may trigger a bank capture in the first place do not come in the limelight. An alternating pattern of liquidity with lows and highs is expected, with the latter occurring at times of asset financial inflow outstripping outflow, where the bank is likely to lend its excess liquidity.

Banks are restricted not to count on the interbank market to clarify all their issues. In their own interest and as expected by bank regulators, they expect to match their assets and liability maturities, something that permits them to sail through stressful market situations.

Market rates could be affected due to the intervention of Central Bank. There can be many factors contributing to it like the change in monetary policy or other factors. This could lead to an increase in market rates or the market may collapse. Depending upon the market problem the banks may have to cut down the client lines.

The Financing Function

As deposits are unfit for the purpose, it is up to capital to provide funds to finance fixed investments (fixed assets and interests in subsidiaries). This particular function is apparent when a bank starts up, when money raised from subscribing shareholders is used to buy buildings, land and equipment. It is desirable to have permanent capital coverage for fixed assets. That means any additional investments in fixed assets should coincide with a capital rise.

During a bank’s life, it generates new capital from its profits. Profits not distributed to shareholders are allocated to other components of shareholders’ equity, resulting in a permanent increase. Capital growth is a source of additional funds used to finance new assets. It can buy new fixed assets, loans or other transactions. It is good for a bank to place some of its capital in productive assets, as any income earned on self-financed assets is free from the cost of borrowed funds. If a bank happens to need more new capital than it can produce itself, it can either issue new shares or take a subordinated debt, both an outside source of capital.

The Restrictive Function

Capital is a widely used reference for limits on various types of assets and banking transactions. The objective is to prevent banks from taking too many chances. The capital adequacy ratio, as the main limit, measures capital against risk-weighted assets.

Depending on their respective relative risks, the value of assets is multiplied by weights ranging from 0 to 20, 50 and 100%. We use the net book value here, reflecting any adjustments, reserves and provisions. As a result, the total of assets is adjusted for any devaluation caused by loan defaults, fixed asset depreciation and market price declines, as the amount of capital has already fallen due to expenses incurred in providing for identified risks. That exposes capital to potential risks, which can lead to future losses if a bank fails to recover its assets.

The minimum required ratio of capital to risk-weighted assets is 8 percent. Under the applicable capital adequacy decree, capital is adjusted for uncovered losses and excess reserves, less specific deductible items. To a limited extent, subordinated debt is also included in capital. The decree also reflects the risks contained in off-balance sheet liabilities.

In the restrictive function context, it is the key importance of capital and the precise determination of its amount in capital adequacy calculations that make it a good base for limitations on credit exposure and unsecured foreign exchange positions in banks. The most important credit exposure limits restrict a bank’s net credit exposure (adjusted for recognizable types of security) against a single customer or a group of related customers at 25% of the reporting bank’s capital, or at 125% if against a bank based in Slovakia or an OECD country. This should ensure an appropriate loan portfolio diversification.

The decree on unsecured foreign exchange positions seeks to limit the risks caused by exchange rate fluctuations in transactions involving foreign currencies, capping unsecured foreign exchange positions (the absolute difference between foreign exchange assets and liabilities) in EUR at 15% of a bank’s capital, or 10% if in any other currency. The total unsecured foreign exchange position (the sum of unsecured foreign exchange positions in individual currencies) must not exceed 25% of a bank’s capital.

The decree dealing with liquidity rules incorporates the already discussed principle that assets, which are usually not paid in banking activities, need to be covered by capital. It requires that the ratio of the sum of fixed investments (fixed assets, interests in subsidiaries and other equity securities held over a long period) and illiquid assets (less readily marketable equity securities and nonperforming assets) to a bank’s own funds and reserves not exceed 1.

Owing to its importance, capital has become a central point in the world of banking. In leading world banks, its share in total assets/liabilities moves between 2.5 and 8 %. This seemingly low level is generally considered sufficient for a sound banking operation. Able to operate at the lower end of the range are large banks with a quality and well-diversified asset portfolio.

Capital adequacy deserves constant attention. Asset growth needs to respect the amount of capital. Eventually, any problems a bank may be facing will show on its capital. In commercial banking, capital is the king.

Bank Management - Basle Norms

The foundation of the Basel banking norms is attributed to the incorporation of the Basel Committee on Banking Supervision (BCBS), established by the central bank of theG-10 countries in 1974. This was under the sponsorship of Bank for International Settlements (BIS), Basel, Switzerland.

The Committee forms guidelines and provides recommendations on banking regulation on the basis of capital risk, market risk and operational risk. The Committee was established in response to the chaotic liquidation of Herstatt Bank, based in Cologne, Germany in 1974. The incident demonstrated the existence of settlement risk in international finance.

Later, this committee was renamed as Basel Committee on Banking Supervision. The Committee acts as a forum where regular collaboration concerning banking regulations and supervisory practices between the member countries takes place. The Committee targets at developing supervisory knowhow and the quality of banking supervision quality worldwide.

Presently, there are 27 member countries in the Committee since 2009. These member countries are being represented in the Committee by the central bank and the authority for the prudential supervision of banking business. Apart from banking regulations and supervisory practices, the Committee also stresses on closing the differences in international supervisory coverage.

Basle I

In 1988, the Basel Committee on Banking Supervision (BCBS) in Basel, Switzerland, announced the first set of minimum capital requirements for banks — Basel I. It completely aimed on credit risk or the default risk. That is the risk of counter party failure. It stated capital need and structure of risk weights for banks.

Under these norms assets of banks were categorized and grouped into five categories according to credit risk, carrying risk weights of 0% like Cash, Bullion, Home Country Debt Like Treasuries, 10, 20, 50 and100% and no rating. Banks with an international presence were expected to hold capital equal to 8% of their risk-weighted assets (RWA). These banks must have at least 4% in Tier I Capital that is Equity Capital + retained earnings and more than 8% in Tier I and Tier II Capital. The target was set to be achieved by 1992.

One of the major functions of Basel norms is to standardize the banking practice across all countries. Anyhow, there are major problems with definition of Capital and Differential Risk Weights to Assets across countries, like Basel standards are computed on the basis of book-value accounting measures of capital, not market values. Accounting practices vary extremely across the G-10 countries and mostly yield outcomes that differ markedly from market assessments.

Another major issue was that the risk weights do not attempt to take account of risks other than credit risks, like market risks, liquidity risks and operational risks that may be critical sources of insolvency exposure for banks.

Basle II

Basel II was introduced in 2004. It speculated guidelines for capital adequacy that is with more refined definitions, risk management like Market Risk and Operational Risk and exposure needs. It also expressed the use of external ratings agencies to fix the risk weights for corporate, bank and sovereign claims.

Operational risk is defined as “the risk of direct and indirect losses resulting from inadequate or failed internal processes, people and systems or from external events”. This comprises of legal risk, but prohibits strategic and reputation risk. Thereby, legal risk involves exposures to fines, penalties, or punitive damages as a result of supervisory actions in addition to private agreements. There are complex methods to appraise this risk.

The exposure needs permit participants of market to evaluate the capital adequacy of the foundation on the basis of information on the scope of application, capital, risk exposures, risk assessment processes, etc.

Basle III

It is believed that the shortcomings of the Basel II norms resulted in the global financial crisis of 2008. That is due to the fact that Basel II norms did not have any explicit regulation on the debt that banks could take on their books, and stressed more on individual financial institutions, while neglecting systemic risks.

To assure that banks don’t take on excessive debt, and that they don’t depend too much on short term funds, Basel III norms were introduced in 2010.The main objective behind these guidelines were to promote a more resilient banking system by stressing on four vital banking parameters — capital, leverage, funding and liquidity.

Needs for mutual equity and Tier 1 capital will be 4.5% and 6%, respectively. The liquidity coverage ratio (LCR) requires the banks to acquire a buffer of high quality liquid assets enough to cope with the cash outflows encountered in an acute short term stress scenario as specified by the supervisors. The minimum LCR need will be to meet 100% on 1 January 2019. This is to secure situations like Bank Run. The term leverage Ratio > 3% denotes that the leverage ratio was calculated by dividing Tier 1 capital by the bank's average total combined assets.

Bank Management - Credit

Credit management is the process of monitoring and collecting payments from customers. A good credit management system minimizes the amount of capital tied up with debtors.

It is very important to have good credit management for efficient cash flow. There are instances when a plan seems to be profitable when assumed theoretically but practical execution is not possible due to insufficient funds. In order to avoid such situations, the best alternative is to limit the likelihood of bad debts. This can only be achieved through good credit management practices.

For running a profitable business in an enterprise the entrepreneur needs to prepare and design new policies and procedures for credit management. For example, the terms and conditions, invoicing promptly and the controlling debts.

Principles of Credit Management

Credit management plays a vital role in the banking sector. As we all know bank is one of the major source of lending capital. So, Banks follow the following principles for lending capital −

Liquidity

Liquidity plays a major role when a bank is into lending money. Usually, banks give money for short duration of time. This is because the money they lend is public money. This money can be withdrawn by the depositor at any point of time.

So, to avoid this chaos, banks lend loans after the loan seeker produces enough security of assets which can be easily marketable and transformable to cash in a short period of time. A bank is in possession to take over these produced assets if the borrower fails to repay the loan amount after some interval of time as decided

A bank has its own selection criteria for choosing security. Only those securities which acquires enough liquidity are added in the bank’s investment portfolio. This is important as the bank requires funds to meet the urgent needs of its customers or depositors. The bank should be in a condition to sell some of the securities at a very short notice without creating an impact on their market rates much. There are particular securities such as the central, state and local government agreements which are easily saleable without having any impact on their market rates.

Shares and debentures of large industries are also addressed under this category. But the shares and debentures of ordinary industries are not easily marketable without having a fall in their market rates. Therefore, banks should always make investments in government securities and shares and debentures of reputed industrial houses.

Safety

The second most important function of lending is safety, safety of funds lent. Safety means that the borrower should be in a position to repay the loan and interest at regular durations of time without any fail. The repayment of the loan relies on the nature of security and the potential of the borrower to repay the loan.

Unlike all other investments, bank investments are risk-prone. The intensity of risk differs according to the type of security. Securities of the central government are safer when compared to the securities of the state governments and local bodies. Similarly, the securities of state government and local bodies are much safer when compared to the securities of industrial concerns.

This variation is due to the fact that the resources acquired by the central government are much higher as compared to resourced held by the state and local governments. It is also higher than the industrial concerns.

Also, the share and debentures of industrial concerns are bound to their earnings. Income varies according to the business activities held in a country. The bank should also consider the ability of the debtor to repay the debt of the governments while investing in their securities. The prerequisites for this are political stability and peace and security within the country.

Securities of a government acquiring large tax revenue and high borrowing capacity are considered as safe investments. The same goes with the securities of a rich municipality or local body and state government of a flourishing area. Thus, while making any sort of investments, banks should decide securities, shares and debentures of such governments, local bodies and industrial concerns which meets the principle of safety.

Therefore, from the bank’s way of perceiving, the nature of security is very essential while lending a loan. Even after considering the securities, the bank needs to check the creditworthiness of the borrower which is monitored by his character, capacity to repay, and his financial standing. Above all, the safety of bank funds relies on the technical feasibility and economic viability of the project for which the loan is to be given.

Diversity

While selecting an investment portfolio, a commercial bank should abide by the principle of diversity. It should never invest its total funds in a specific type of securities, it should prefer investing in different types of securities.

It should select the shares and debentures of various industries located in different parts of the country. In case of state governments and local governing bodies, same principle should be abided to. Diversification basically targets at reducing risk of the investment portfolio of a bank.

The principle of diversity is applicable to the advancing of loans to different types of firms, industries, factories, businesses and markets. A bank should abide by the maxim that is “Do not keep all eggs in one basket.” It should distribute its risks by lending loans to different trades and companies in different parts of the country.

Stability

Another essential principle of a bank’s investment policy is stability. A bank should prefer investing in those stocks and securities which hold a high degree of stability in their costs. Any bank cannot incur any loss on the rate of its securities. So it should always invest funds in the shares of branded companies where the probability of decline in their rate is less.

Government contracts and debentures of industries carry fixed costs of interest. Their cost varies with variation in the market rate of interest. But the bank is bound to liquidate a part of them to satisfy its needs of cash whenever stuck by a financial crisis.

Else, they follow their full term of 10 years or more and variations in the market rate of interest do not disturb them. So, bank investments in debentures and contracts are more stable when compared to the shares of industries.

Profitability

This should be the chief principle of investment. A bank should only invest if it earns sufficient profits from it. Thus, it should, invest in securities that have a fair and stable return on the funds invested. The procuring capacity of securities and shares relies on the interest rate and the dividend rate and the tax benefits they hold.

Broadly, it is the securities of government branches like the government at the center, state and local bodies that hugely carry the exception of their interest from taxes. A bank should prefer investing in these type of securities instead of investing in the shares of new companies which also carry tax exception. This is due to the fact that shares of new companies are not considered as safe investments.

Now lending money to someone is accompanied by some risks mainly. As we know that bank lends the money of its depositors as loans. To put it simply the main job of a bank is to rent money from depositors and give money to the borrowers. As the primary source of funds for a bank is the money deposited by its customers which are repayable as and when required by the depositors, the bank needs to be very careful while lending money to customers.

Banks make money by lending money to borrowers and charging some interest rates. So, it is very essential from the bank’s part to follow the cardinal principles of lending. When these principles are abided, they assure the safety of banks’ funds and in response to that they assure its depositors and shareholders. In this whole process, banks earn good profits and grow as financial institutions. Sound lending principles by banks also help the economy of a nation to prosper and also advertise expansion of banks in rural areas.

Bank Management - Formulating Loan Policy

Basically, loan portfolios have the largest effect on the total risk profile and earnings performance. This earning performance comprises of various factors like interest income, fees, provisions, and other factors of commercial banks.

The mediocre loan portfolio marks approximately 62.5 percent of total centralized assets for banking organizations with less than $1 billion in total assets and 64.9 percent of total centralized assets for banking organizations with less than $10 billion in total assets.

In order to limit credit risk, it is compulsory that suitable and effective policies, procedures, and practices are developed and executed. Loan policies should coordinate with the target and objectives of the bank, in addition to supporting safe and sound lending activity.

Policies and procedures should be presented as a layout for all major credit decisions and actions, enclosing all material aspects of credit risk, and mirroring the complexity of the activities in which a bank is engaged.

Policy Development

As we know risks are inevitable, banks can lighten credit risk by development of and cohesion to efficient and effective loan policies and procedures. A well-documented and descriptive loan policy proves to be the milestone of any sound lending function.

Ultimately, a bank’s board of directors is accountable for flaying out the structure of the loan policies to address the inherent and residual risks. Residual risks are those risks that remain even after sound internal controls have been executed in the lending business lines.

After formulating the policy, senior management is held accountable for its execution and ongoing monitoring, accompanied by the maintenance of procedures to assure they are up to date and compatible to the current risk profile.

Policy Objectives

The loan policy should clearly communicate the strategic goals and objectives of the bank, as well as define the types of loan exposures acceptable to the institution, loan approval authority, loan limits, loan underwriting criteria, and several other guidelines.

It is important to note that a policy differs from procedures in which it sets forth the plan, guiding principles, and framework for decisions. Procedures, on the other hand, establish methods and steps to perform tasks. Banks that offer a wider variety of loan products and/or more complex products should consider developing separate policy and procedure manuals for loan products.

Policy Elements

The regulatory agencies’ examination manuals and policy statements can be considered as the best place to begin when deciding the key elements to be incorporated into the loan policy.

In order to outline loan policy elements, the bank should have a consistent lending strategy, identifying the types of loans that are permissible and those that are impermissible. Along with identifying the types of loans, the bank will and will not underwrite regardless of permissibility. The policy elements should also outline other common loan types found in commercial banks.

The major policy elements for a bank are −

- A statement highlighting the features of a good loan portfolio in terms of types, maturities, sizes, and quality of loans. In short, a goal statement for entire loan portfolio.

- Stipulation of lending authority prescribed to each loan officer and loan committee. The main task of loan officers and loan committee is to measure the maximum amount and types of loan approved by each employee and committee and what signatures of approval are needed.

- Boundaries of duty in making assignments and reporting information.

- Functioning procedures for soliciting, examining, accessing and making decisions on customer loan applications.

- The documents required for each loan application and all the necessary papers and records to be kept in the lender’s files like financial statements, pass book details, security agreements, etc.

- Lines of authority and accountability for maintaining, monitoring, updating and reviewing the institution’s credit files.

Loan policies vary significantly from one bank to another. It is completely based on the complexity of the activities they are engaged in. The policy elements of a private bank may slightly differ from the government bank. Anyhow, a general loan policy incorporates specific basic lending tenets.

Bank Mngmt - Asset Liability

Asset liability management is the process through which an association handles its financial risks that may come with changes in interest rate and which in turn would affect the liquidity scenario.

Banks and other financial associations supply services which present them to different kinds of risks. We have three types of risks — credit risk, interest risk, and liquidity risk. So, asset liability management is an approach or a step that assures banks and other financial institutions with protection that helps them manage these risks efficiently.

The model of asset liability management helps to measure, examine and monitor risks. It ensures appropriate strategies for their management. Thus, it is suitable for institutions like banks, finance companies, leasing companies, insurance companies, and other financing bodies.

Asset liability management is an initial step to be taken towards the long term strategic planning. This can also be considered as an outlining function for an intermediate term.

In particular, liability management also refers to the activities of purchasing money through cumulative deposits, federal funds and commercial papers so that the funds lead to profitable loan opportunities. But when there is an increase of volatility in interest rates, there is major recession damaging multiple economies. Banks begin to focus more on the management of both sides of the balance sheet that is assets as well as liabilities.

ALM Concepts

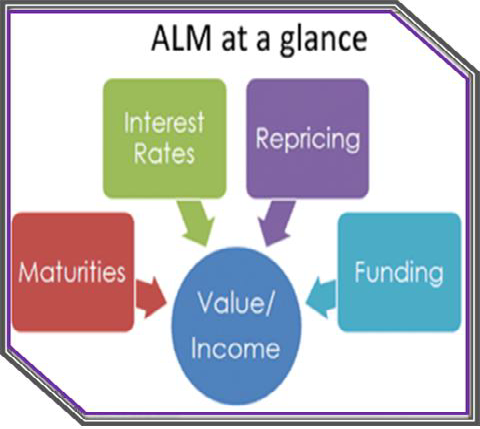

Asset liability management (ALM) can be stated as the comprehensive and dynamic layout for measuring, examining, analyzing, monitoring and managing the financial risks linked with varying interest rates, foreign exchange rates and other elements that can have an impact on the organization’s liquidity.

Asset liability management is a strategic approach of managing the balance sheet in such a way that the total earnings from interest are maximized within the overall risk-preference (present and future) of the institutions.

Thus, the ALM functions include the tools adopted to mitigate liquidly risk, management of interest rate risk / market risk and trading risk management. In short, ALM is the sum of the financial risk management of any financial institution.

In other words, ALM handles the following three central risks −

- Interest Rate Risk

- Liquidity Risk

- Foreign currency risk

Banks which facilitate forex functions also handles one more central risk — currency risk. With the support of ALM, banks try to meet the assets and liabilities in terms of maturities and interest rates and reduce the interest rate risk and liquidity risk.

Asset liability mismatches − The balance sheet of a bank’s assets and liabilities are the future cash inflows & outflows. Under asset liability management, the cash inflows & outflows are grouped into different time buckets. Further, each bucket of assets is balanced with the matching bucket of liability. The differences obtained in each bucket are known as mismatches.

Bank Management - Evolution Of ALM

There was no significant interest rate risk during the 1970s to early 1990s period. This is because the interest rates were formulated and recommended by the RBI. The spreads between deposits and lending rates were very wide.

In those days, banks didn’t handle the balance sheets by themselves. The main reason behind this was, the balance sheets were managed through prescriptions of the regulatory authority and the government. Banks were given a lot of space and freedom to handle their balance sheets with the deregulation of interest rates. So, it was important to launch ALM guidelines so that banks can remain safe from big losses due to wide ALM mismatches.

The Reserve Bank of India announced its first set of ALM Guidelines in February 1999. These guidelines were effective from 1st April, 1999. These guidelines enclosed, inter alia, interest rate risk and liquidity risk measurement, broadcasting layout and prudential limits. Gap statements were necessary to be made by scheduling all assets and liabilities according to the stated or anticipated re-pricing date or maturity date.

At this stage the assets and liabilities were enforced to be divided into the following 8 maturity buckets −

- 1-14 days

- 15-28 days

- 29-90 days

- 91-180 days

- 181-365 days

- 1-3 years

- 3-5 years

- and above 5 years

On the basis of the remaining intervals to their maturity which are also referred as residual maturity, all the liability records were to be studied as outflows while the asset records were to be studied as inflows.

As a measure of liquidity management, banks were enforced to control their cumulative mismatches beyond all time buckets in their statement of structural liquidity by building internal prudential limits with the consent of their boards/ management committees.

According to the prescribed guidelines, in the normal course, the mismatches also known as the negative gap in the time buckets of 1-14 days and 15-28 days were not to cross 20 per cent of the cash outflows with respect to the time buckets.

Later, the RBI made it compulsory for banks to form ALCO, that is, the Asset Liability Committee as a Committee of the Board of Directors to track, control, monitor and report ALM.

This was in September 2007, in response to the international exercises and to satisfy the requirement for a sharper evaluation of the efficacy of liquidity management and with a view to supplying a stimulus for improvement of the term-money market.

The RBI fine-tuned these regulations and it was ensured that the banks shall accept a more granular strategy for the measurement of liquidity risk by dividing the first time bucket that is of 1-14 days currently in the Statement of Structural Liquidity into three time buckets. They are 1 day addressed next day, 2-7 days and 8-14 days. Hence, banks were demanded to put their maturing asset and liabilities in 10 time buckets.

According to the RBI guidelines announced in October 2007, banks were recommended that the total cumulative negative mismatches during the next day, 2-7 days, 8-14 days and 15-28 days should not cross 5%, 10%, 15% and 20% of the cumulative outflows, respectively, in order to address the cumulative effect on liquidity.

Banks were also recommended to attempt dynamic liquidity management and design the statement of structural liquidity on a regular basis. In the absence of a fully networked environment, banks were permitted to assemble the statement on best present data coverage originally but were advised to make careful attempts to attain 100 per cent data coverage in a timely manner.

In the same manner, the statement of structural liquidity was to be presented to the RBI at regular intervals of one month, as on the third Wednesday of every month. The frequency of supervisory reporting on the structural liquidity status was changed to fortnightly, with effect from April 1, 2008. The banks are expected to acknowledge the statement of structural liquidity as on the first and third Wednesday of every month to the Reserve Bank.

Boards of the Banks were allocated with the complete duty of the management of risks and were needed to conclude the risk management policy and set limits for liquidity, interest rates, foreign exchange and equity price risks.

The Asset-Liability Committee (ALCO) is one of the top most committees to overlook the execution of ALM system. This committee is led by the CMD/ED. ALCO also acknowledges product pricing for the deposits as well as the advances. The expected maturity profile of the incremental assets and liabilities along with controlling, monitoring the risk levels of the bank. It needs to mandate the current interest rates view of the bank and base its decisions for future business strategy on this view.

The ALM Process

The ALM process rests on the following three pillars −

- ALM information systems

- Management Information System

- Information availability, accuracy, adequacy and expediency

It comprises of functions like identifying the risk parameters, identifying the risk, risk measurement and Risk management and laying out of Risk policies and tolerance levels.

ALM information systems

The key to the ALM process is information. The large network of branches and the unavailability an adequate system to collect information necessary for ALM, which examines information on the basis of residual maturity and behavioral pattern makes it time-consuming for the banks in the current state to procure the necessary information.

Measuring and handling liquidity requirements are important practices of commercial banks. By persuading a bank’s ability to satisfy its liabilities as they become due, the liquidity management can minimize the probability of an adverse situation developing.

The Importance of Liquidity

Liquidity go beyond individual foundations, as liquidity shortfall in one foundation can have backlash on the complete system. Bank management should not only portion the liquidity designations of banks on an ongoing basis but also analyze how liquidity demands are likely to evolve under crisis scenarios.

Past experience displays that assets commonly assumed as liquid like Government securities and other money market tools could also become illiquid when the market and players are Unidirectional. Thus liquidity has to be chased through maturity or cash flow mismatches.

Bank Management - Risks With Assets